Robert Magan, CFA®

Senior Vice President

Senior Wealth Management Officer

603.230.4219

04/02/2026

The stock market thus far in 2026 has begun in similar fashion to 2025, with profit-taking in many of the large technology stocks along with a renewed interest in other industries and international markets. One year ago, in February and March, consolidation among the Magnificent 7 group of stocks collapsed into a bear market; the S&P 500 index declined 19% and the NASDAQ index fell more than 25% in response to ‘Liberation Day’ tariffs announced in early April. Fortunately, last year’s sell-off was short-lived, and the market regained its footing.

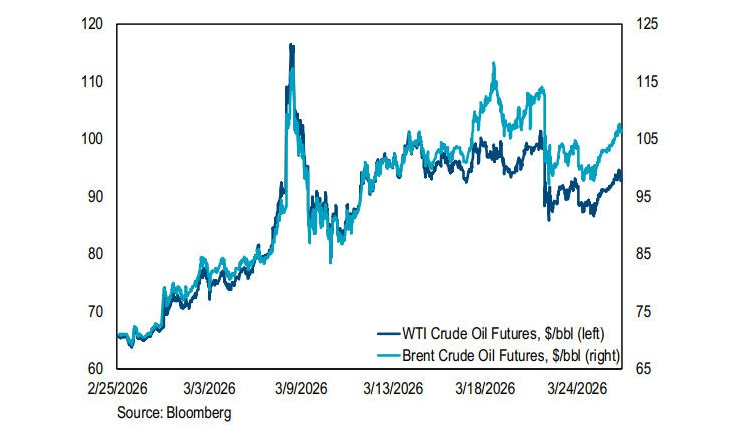

This year, the conflict in Iran is at the forefront of news, but its effect has thus far been limited to substantial increases in global crude oil and fertilizer prices. The sharp sell- off in major software companies has been attributed to fears of obsolescence from the development and implementation of artificial intelligence rather than from news in the Middle East. Despite a 27% decline in a broad index of Tech software companies as of March 31, the S&P 500 is down 4.6%, supported by stronger performance in other sectors.

We anticipate heightened volatility and continued selling pressure as the correction runs its course in the short term, and it’s possible the market will continue to follow a pattern similar to last year, reaching a point of panic before resuming its upward trend. These volatile periods can provide opportunities to add to positions at lower prices, proving beneficial in the long term. Investors who participated in panic selling during the lows in 2025 may have realized double-digit losses, but those who maintained discipline by remaining invested were rewarded with double-digit gains.

Free elections are a hallmark of democratic societies, secured through hard-fought rights won with great sacrifice. Elections introduce increased uncertainty and volatility to the markets which creates unease for investors. The general public is bombarded with political ads and talking heads that create confusion. While some years have experienced less, history has shown the average drawdown during midterm elections to be 19% from the closing high to the closing low. In the previous midterm in 2022, the market fell 25% during a cycle of the Fed raising interest rates, however, it ultimately settled at a more palatable loss of 18%. In many cases the market tends to make a low during the summer and subsequently begins to recover as the election approaches. The magnitude of the correction in any given year is influenced by many things including Fed monetary policy, the state of the economy and market valuation. Based on the historical pattern, we expected profit-taking among the better-performing stocks and consolidation in the market as a whole. This year, it began in mid-February, even prior to military strikes on Iran, and the correction may run its course sooner than it typically does in late summer. The good news is that in most midterm years the market finishes with positive returns, and we expect 2026 to do so as well.

The Unknowns

The market has been sanguine towards conflict in Iran, likely based on the expectation of limited duration. Admittedly, the latest news of potential escalation or de-escalation exacerbates volatility on any given day. The larger question becomes the issue of higher oil and fertilizer prices and how long they remain elevated after settlement talks and the eventual reopening of the Strait of Hormuz.

Our base case in January was for another positive year in global equity markets supported by steady economic growth and tame inflation. The consequences of the military action may result in higher prices for longer than expected. The effect on the consumer from higher food and energy costs could lead to slower economic growth and reduce the earnings outlook for many business sectors. Earnings for the S&P 500 index are estimated to increase by 16% in 2026 based on the assumption of earnings growth accelerating in the second-half of the year. This outlook may prove to be optimistic and could create additional volatility or limit the upside during a stock market recovery.

The Net Result

We believe much of the stock market correction has already occurred, stock prices will likely trade in a narrow range over several weeks, creating a bottom. We expect estimates for economic and earnings growth to be revised lower but do not expect a recession to ensue. Fed Chairman Jay Powell has stated the Fed will not raise rates due to inflation caused by the crude oil supply shock, and our outlook for two rate cuts this year is now much more dependent on employment data as the year unfolds. While conditions seem less clear today than a few months ago, we do not see the need for large shifts in asset allocation out of equities. Many domestic and international companies continue to innovate and thrive, and in some cases, valuation has become more attractive. Diversification remains paramount to managing portfolio risk, and we strive to attain that by avoiding excessive concentration in individual sectors or asset classes. Much like the early part of last year, bond investments have reduced volatility and provided income during a period of temporary weakness in stocks. We are reminded that stock prices fluctuate and rarely stop at ‘fair value’ in either direction but rather deliver attractive returns over longer investment periods. We continue to monitor conditions and will make prudent adjustments as needed.

We are grateful for the opportunity to serve many families and organizations in NH, New England and beyond. Please reach out with questions or if changes in your needs arise. We are here for you.

Robert Magan, CFA®

Senior Vice President

Senior Wealth Management Officer

603.230.4219

Steve Smith, CFA®

Senior Vice President

Wealth Advisor/Strategist

603.230.4209

Dona G. Murray

Senior Vice President

Wealth Advisor

603.527.3936

Paul R. Zepf, CFA®

Vice President

Wealth Advisor

603.527.3234

Securities and Insurance Products are:

| Not FDIC Insured | Not Bank Guaranteed | May Lose Value | Not a Deposit | Not Insured by any Government Agency |